Laying the Groundwork

This post assumes the Comparable Profits Method (CPM) is the best method under 1.482-1(c), with operating margin after depreciation (OMAD) as the profit indicator (PLI). The key question addressed in this post is whether the operating income from a comparable reflects its recurring economics or is distorted by an impairment charge that should be excluded from the analysis. Additionally, we’ll consider in Section III whether a charge belongs in operating income but compresses the arm’s length range, requiring an adjustment.

A CPM analysis typically involves gathering operating income for comparables, calculating margins, establishing an arm’s-length range, and benchmarking the tested party. It becomes complicated when a comparable’s reported income doesn’t reflect true economics. For example, a company with a $2 billion goodwill write-down has a margin that doesn’t match its recurring costs, and one with frequent impairment charges reports margins that mix charge and recovery periods. Relying on these figures can produce a range that reflects accounting noise rather than real economic performance.

The regulations anticipate this problem. 1.482-5(c)(2)(iv) states that if differences between the tested party and an uncontrolled comparable materially affect profits, adjustments should be made. The determination to be made is whether a reported impairment is the kind of difference this provision covers, based on its origin, classification, and whether the industry has a history of similar charges.

The codification allows companies to allocate impairment charges flexibly on the income statement. Combined with incentives for earnings management, this makes operating income a variable measure across the comparable set, often unclear until examined closely.

I. The Governing Codification

Three ASC subtopics do the substantive work in this area, and it is worth briefly walking through each before turning to the income statement presentation rules.

350-30 (Intangibles Other Than Goodwill) is the central subtopic. It governs useful life determination (finite vs. indefinite), the amortization of finite-lived intangibles under 350-30-35-6 through 35-13, and the annual impairment test for indefinite-lived intangibles under 350-30-35-15 through 35-22. Finite-lived intangibles, such as customer relationships, developed technology, patents, non-compete agreements, and licensed know-how, are amortized over their useful lives and tested for impairment under the 360-10 model when a triggering event occurs. Indefinite-lived intangibles, by contrast — trade names, certain perpetual licenses — are not amortized at all. They are tested at least annually under 350-30-35-18 and 35-19 by comparing fair value to carrying amount, with any excess of carrying amount over fair value recognized as an impairment loss. Reversal of a previously recognized loss is not permitted (350-30-35-20).

350-20 (Goodwill) governs the subsequent accounting for goodwill acquired in a business combination under ASC 805, and the rules differ between public and private companies that sometimes affect our analyses. Public companies, rather than amortizing goodwill, test it for impairment at least annually (and more frequently if triggering events arise) at the reporting unit level under 350-20-35-28 and 35-30. Accounting Standards Update (ASU) 2017-04 streamlined the impairment test to a single step: if the reporting unit’s carrying amount exceeds its fair value, the entity recognizes a loss equal to that excess, not to exceed the balance of goodwill allocated to the reporting unit.

360-10 (Impairment of Long-Lived Assets) prescribes the impairment model for long-lived assets held and used, including finite-lived intangibles, in 360-10-35-17 through 35-35. The model is trigger-based. The entity first compares the asset group’s carrying amount to its undiscounted future cash flows — the recoverability test — and, only if the carrying amount is not recoverable, measures the impairment loss as the excess of the carrying amount over fair value (360-10-35-17). The loss is allocated pro rata to the group’s long-lived assets (360-10-35-28).

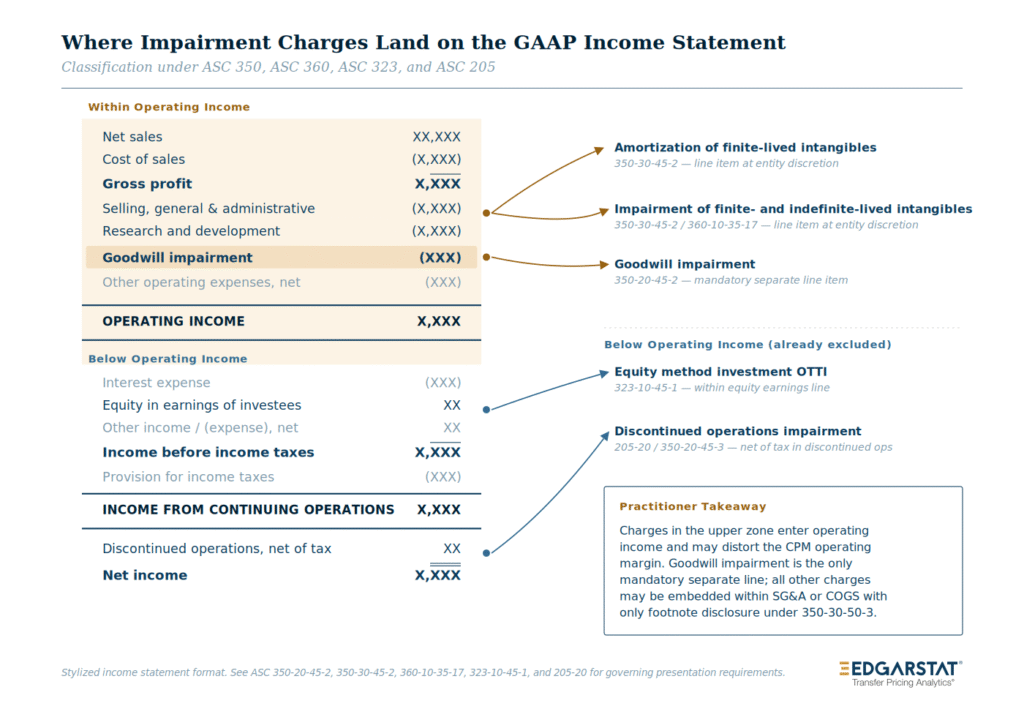

II. Income Statement Presentation: Within or Below Continuing Operations

What matters is where each charge appears on the GAAP income statement, specifically if it is deducted to arrive at operating income (above or below the line). This line decides whether the charge affects the OMAD.

| Charge Type | Governing ASC | Presentation | Separate Line Required? |

|---|---|---|---|

| Amortization of finite-lived intangibles | 350-30-45-2 | Within continuing operations | No, entity discretion |

| Impairment of finite-lived intangibles | 360-10-35-17 / 350-30-45-2 | Within continuing operations | No, entity discretion |

| Impairment of indefinite-lived intangibles | 350-30-45-2 | Within continuing operations | No, entity discretion |

| Goodwill impairment | 350-20-45-2 | Within continuing operations | Yes, mandatory separate line |

| Discontinued operations impairment | 350-20-45-3 | Below continuing operations | N/A, net of tax within discontinued operations |

The table’s asymmetry appears in the last column, where goodwill impairment is the only intangible charge required to be presented separately. Other charges can be included in cost of sales, SG&A, or other operating lines, with footnotes indicating their source.

Charges Within Continuing Operations

Amortization of finite-lived intangibles. 350-30-45-2 states that amortization expense “shall be presented in income statement line items within continuing operations as deemed appropriate for each entity,” leaving the line item to the entity’s discretion. In 2008, a registrant told the SEC that ASC 350 “does not require that amortization of acquired intangible assets be allocated to any specific cost category,” which the SEC accepted, requiring only disclosure that the cost of revenue lines are “exclusive of amortization of intangible assets, which is shown separately below.” Consequently, two similar companies can report different operating margins due to presentation choices — one allocating amortization to cost of revenue, the other as a separate line item. Identifying this requires careful reading of each company’s disclosures.

Impairment of intangible assets (finite-lived and indefinite-lived). The same provision (350-30-45-2) covers amortization and impairment losses, which “shall be presented in income statement line items within continuing operations” as appropriate. The only identification requirement is the footnote disclosure by 350-30-50-3. An entity can present a large trade name impairment in SG&A and still meet GAAP if footnotes disclose it.

Goodwill impairment. Goodwill impairment is the easiest to identify, mainly because 350-20-45-2 requires separate-line presentation, eliminating the need to check footnotes. The economic content of goodwill differs from operating costs the tested party would incur under arm’s length conditions. The impairment writes down premiums embedded in the purchase price allocation, which an independent company without similar acquisitions wouldn’t have. Adding the charge back to operating income is supported by the SEC, which enforces the separate-line rule against hiding goodwill impairments in SG&A, so we can usually rely on the income statement itself rather than footnotes. regulations and economics.

Long-lived asset impairment under 360-10. Finite-lived intangible impairment under 360-10 is shown within continuing operations per 350-30-45-2. It need not be separated, so footnote review remains essential.

Charges Outside Continuing Operations

Equity method investment impairment (ASC 323). 323-10-45-1 requires that the investor’s share of earnings or losses from an equity method investment be presented as a single line item on the income statement, typically below operating income but within income from continuing operations. Any impairment of the equity method investment other than temporary is recognized in that line, so it does not affect reported operating income.

Discontinued operations. 350-20-45-3 routes goodwill impairment associated with a discontinued operation, net of tax, into the results of discontinued operations; this means the amount does not affect reported operating income. The same treatment applies when a long-lived asset group satisfies the held-for-sale criteria under 360-10-45-9, and the disposal group is a discontinued operation, in which case any write-down is reported outside of operating income.

III. Impairment Charges and the Arm’s Length Range

How the Distortion Works

When a comparable in our CPM analysis incurs a material, nonrecurring impairment charge in operating income, the margin won’t reflect that comparable’s recurring economics. The distortion is mostly mechanical. The charge compresses the low end of the arm’s length range when it hits, and since impaired assets no longer generate amortization, it expands the high end in future years. This results in a margin profile that doesn’t accurately show either the charge or recovery period economics — a distorted middle ground unhelpful for our benchmarking.

The problem worsens when considering earnings management. Schilit and Perler, in Financial Shenanigans (4th ed.), describe classification techniques companies use to inflate operating income. One key method is “shifting normal operating expenses (i.e., the ‘bad stuff’) to the nonoperating section.” They explain that a company could take a one-time charge, like writing off inventory or assets, and move related expenses (cost of goods sold or depreciation) from the Operating to the nonoperating section, boosting operating income. Intangible write-downs, like restructuring charges, follow the same idea: absorbing future amortization into current below-the-line charges, leaving later periods with inflated income. Schilit and Perler call this a “win-win situation for the company: operating income (above the line) in the period of the charge is unaffected since the impact is felt below the line; and operating income in the later period is inflated as normal expenses have been pulled out and included in the earlier-period charge.”

The Big Bath

Fridson and Alvarez describe a related earnings management technique in Financial Statement Analysis (5th ed.). When a company’s earnings decline too much to offset with ordinary items, management may “accelerate certain future expenses into the current quarter, thereby ensuring positive reported earnings in the following period.” The logic the authors attribute to management is blunt: companies take outsized write-downs on “outmoded production facilities and goodwill created in unsuccessful acquisitions” because “investors will not be much more disturbed by a 30 percent drop in earnings than by a 20 percent drop.” The bath year tanks the five-year weighted average operating margin, with recovery years (lower amortization base) raising it. The five-year average doesn’t reveal if either event occurred, risking silent distortion when evaluating a comparable with a bad year mid-period.

Recurring “Nonrecurring” Charges

Eastman Kodak recorded restructuring charges in 18 of 23 years that Fabozzi and Peterson Drake examined in Analysis of Financial Statements (3rd ed.), which the authors describe as the kind of pattern in which “nonrecurring and extraordinary items have become quite ordinary, reporting gains and losses each year arising from these sources.” Alcatel, according to Schilit and Perler, recorded below-the-line restructuring charges “in just about every quarter since the early 1990s.”

The SEC, weary of this trend among registrants, challenged Whirlpool in a September 2016 comment letter, asking the company to “explain to us why these are not normal, recurring, cash operating expenses necessary to operate your business.”

Cookie Jar Reserves

Zack, in Financial Statement Fraud, covers another angle relevant to our analysis: the use of reserve accounts to smooth earnings across periods. Cardinal Health, for example, maintained “no less than 60 different reserve accounts” and, according to SEC charges, “inflated its earnings by more than $65 million” through improper manipulation between 2000 and 2004. This construct occurs when an entity overestimates an impairment charge or restructuring reserve, then releases the excess into income later to boost earnings.

The Regulatory Framework for Adjustments

The regulatory provision for addressing these distortions is section 1.482-5(c)(2)(iv), which provides that “[i]f there are differences between the tested party and an uncontrolled comparable that would materially affect the profits determined under the relevant profit level indicator, adjustments should be made according to the comparability provisions of 1.482-1(d)(2).” The same provision goes on to note that “[i]n certain cases it may also be appropriate to adjust the operating profit of the tested party and comparable parties,” which is a useful reminder that the adjustment can move in either direction. The parent provision, 1.482-1(d)(2), provides the standard: “adjustments must be made if the effect of such differences on prices or profits can be ascertained with sufficient accuracy to improve the reliability of the results.” A nonrecurring, acquisition-driven impairment charge that is separately disclosed on the face of the income statement (or in the footnotes under 350-30-50-3 or 350-20-50-2) clears this bar of ascertainability, because we can read the amount directly from the footnote disclosures and add it back to operating income.

Beyond ascertainability, the decision to adjust reported operating income is fact-specific. Recurrence is the primary filter. A single goodwill impairment after a failed acquisition should be reclassified as non-operating, but if such charges recur across many periods, adjusting them might distort rather than correct.

The next filter considers whether the charge is entity-specific or market-wide. An impairment triggered by an entity-specific event, like a failed product launch or a terminated license, affects one company, not the whole industry, and warrants adjustment since the tested party wouldn’t have incurred it under arm’s length conditions. An industry-wide impairment, however, may reflect conditions the tested party also faces, so leaving it in operating income might be appropriate. These are judgments, but they should be well-structured and supported by facts.

Charges outside income from continuing operations require no further action on our part. Equity method impairments and discontinued operations fall here; adjustments are only for charges initially classified within operating income.

Common Adjustments

Goodwill impairment is the clearest adjustment, as 350-20-45-2 makes the charge obvious and because the underlying economic content of goodwill is not the kind of thing the tested party would incur as an arm’s length operating cost. Adding it back to operating income is well-supported.

Acquisition-related intangible amortization is a broader question, particularly in industries where M&A activity is routine. Amortization can be a significant component of operating expenses in such industries. If the tested party has not made comparable acquisitions, adjusting for acquired intangible amortization across both the tested party and the comparable set may produce a more reliable measure.

Restructuring charges that bundle intangible write-downs with severance and exit costs are the hardest to analyze because they need to be broken down first. The Whirlpool letter serves as a useful example in determining whether the charge recurs periodically (suggesting it’s a recurring operating expense disguised as a one-time event) or is a discrete, nonoperating event.

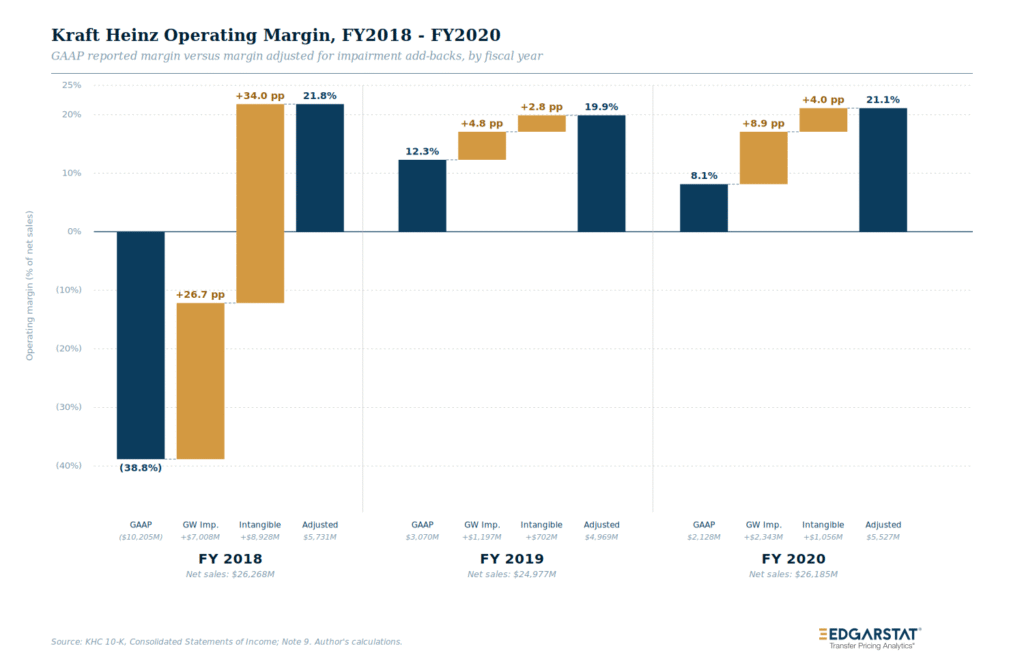

IV. Case Study: The Kraft Heinz Company, Fiscal Year 2020

The Kraft Heinz 10-K for the fiscal year ended December 26, 2020, highlights numerous distortions. KHC is a multinational food and beverage company with over $26 billion in net sales across three segments — 73% U.S., 20% International, 6% Canada. Its intangible assets mainly stem from the 2013 Heinz acquisition by 3G Capital and Berkshire Hathaway, and the 2015 Kraft-Heinz merger. These transactions created $33.1 billion in goodwill and $42.3 billion in indefinite-lived intangibles as of December 26, 2020, making KHC’s reported operating income sensitive to future impairment charges.

GAAP Operating Income vs. Adjusted Operating Performance

KHC presents both goodwill impairment losses and intangible asset impairment losses as separate line items within SG&A, both of which sit inside reported operating income:

| Fiscal Year | Net Sales | Goodwill Impairment | Intangible Asset Impairment | Total Impairment | GAAP Operating Income/(Loss) |

|---|---|---|---|---|---|

| 2020 | $26,185M | $2,343M | $1,056M | $3,399M | $2,128M |

| 2019 | $24,977M | $1,197M | $702M | $1,899M | $3,070M |

| 2018 | $26,268M | $7,008M | $8,928M | $15,936M | ($10,205M) |

(Source: KHC 10-K, Consolidated Statements of Income; Note 9.)

If we add the impairment losses back to reported GAAP operating income, the picture changes entirely:

| Fiscal Year | GAAP Operating Margin | Adjusted Operating Margin (ex-impairments) |

|---|---|---|

| 2020 | 8.1% | 21.1% |

| 2019 | 12.3% | 19.9% |

| 2018 | (38.8%) | 21.8% |

(Author’s calculations from KHC 10-K data.)

GAAP figures fluctuate from -38.8% to 12.3% and 8.1%, while adjusted figures stay near 20-22%. This shows the company’s core economics are stable despite volatile GAAP OMAD. An analyst using unadjusted figures for comparison would see margins disconnected from actual costs, resulting in a range influenced by acquisition accounting rather than true economics.

KHC’s Own Non-GAAP Reconciliation

KHC considers these impairment charges not indicative of core performance, and their Adjusted EBITDA excludes these losses, citing they “do not directly reflect our underlying operations” (KHC 2020 10-K, Non-GAAP Financial Measures).

| Item | Amount (FY 2020) |

|---|---|

| GAAP Operating income/(loss) | $2,128M |

| Depreciation and amortization | $955M |

| Integration and restructuring expenses | $15M |

| Deal costs | $8M |

| Unrealized gains on commodity hedges | ($6M) |

| Impairment losses | $3,413M |

| Equity award compensation expense | $156M |

| Adjusted EBITDA | $6,669M |

(Source: KHC 2020 10-K, Reconciliation of Net Income/(Loss) to Adjusted EBITDA.)

Impairment losses account for about 75% of the difference between GAAP operating income and Adjusted EBITDA, highlighting the distortion. The company’s Adjusted EPS attributes $2.59 (2020) and $1.38 (2019) per share to impairment losses, compared to GAAP EPS of $0.29 and $1.58. The company asserts that these charges should be excluded from assessments of operating performance. If KHC makes this point to shareholders, it should also influence our transfer pricing analysis, focusing on the company’s recurring operating performance.

The Impairments Are Acquisition-Driven

KHC links every recorded impairment to purchase price allocations from 2013 and 2015 transactions, as detailed in Note 9. The company states that even brands with over 50% excess fair value over carrying amount are tied to past acquisitions — specifically, the 2013 Heinz purchase and the 2015 merger — and are recorded at their acquisition date fair values. Consequently, they remain vulnerable to impairments. KHC attributes the 2020 goodwill impairments to entity-specific events like a new strategy, reorganization, and COVID-19 impacts, which are reassessments of prior valuations rather than typical operating costs.

The 2020 goodwill impairments were allocated as follows: $655M in the United States (U.S. Foodservice), $368M in International (ANJ, LATAM, and EMEA East), and $1,020M in Canada (Canada Retail and Canada Foodservice). The indefinite-lived intangible asset impairments totaled $1,056M, with most of that attributable to Oscar Mayer at $626M and Maxwell House at $140M, and the remaining $290M distributed across Velveeta, Cool Whip, Plasmon, ABC, Classico, Wattie’s, and Planters (KHC 10-K, Note 9).

Recurring “Nonrecurring”: The Three-Year Pattern

KHC recorded annual impairment charges from 2018 to 2020, totaling $21.2 billion. By December 26, 2020, four reporting units had fair value just over 10% of their carrying amounts (with $7.5 billion in goodwill), and eleven brands had less than 1% excess fair value (with $21.8 billion in carrying amounts). The 10-K states that units and brands with 20% or less excess fair value face a higher risk of future impairments, indicating this pattern may continue. The SEC has issued subpoenas regarding KHC’s impairment assessments, highlighting the need for scrutiny of these judgments.

V. Practical Guidance

When analyzing comparable sets, we start with each income statement to find impairment and amortization line items. If none are found, we check footnotes, as non-goodwill impairments are usually hidden in SG&A or cost of sales, with details in the 350-30-50-3 footnote. These disclosures provide the asset description, circumstances, loss amount, and relevant income statement caption, whether for non-goodwill (350-30-50-3) or goodwill (350-20-50-2).

Takeaways

The codification allows companies broad discretion on where impairment and amortization charges are shown on the GAAP income statement, with the only mandatory separate line for goodwill impairment under 350-20-45-2. This discretion, along with incentives for big baths and cookie-jar accounting, means reported operating income isn’t always a reliable benchmark of arm’s length profitability. Kraft Heinz exemplifies this, with $21.2 billion in impairments over three years — all within operating income — yet maintaining a stable 20-22% adjusted operating margin used to show performance. In transfer pricing, we must identify which impairment charges are genuine economic events and which are distortions needing adjustments under 1.482-5(c)(2)(iv). The codification tells us where charges are reported, and disclosures explain why. Our task is to decide whether they should stay there for our analysis.

References

Fabozzi, Frank J., and Pamela Peterson Drake. Analysis of Financial Statements. 3rd ed. Hoboken, NJ: John Wiley & Sons, 2012.

Fridson, Martin S., and Fernando Alvarez. Financial Statement Analysis: A Practitioner’s Guide. 5th ed. Hoboken, NJ: John Wiley & Sons, 2022.

Schilit, Howard M., Jeremy Perler, and Yoni Engelhart. Financial Shenanigans: How to Detect Accounting Gimmicks and Fraud in Financial Reports. 4th ed. New York: McGraw-Hill Education, 2018.

Zack, Gerard M. Financial Statement Fraud: Strategies for Detection and Investigation. Hoboken, NJ: John Wiley & Sons, 2013.

Whirlpool Corporation. Letter from Larry M. Venturelli, Executive Vice President and Chief Financial Officer, to Carlos Pacho, Senior Assistant Chief Accountant, U.S. Securities and Exchange Commission, Division of Corporation Finance (Form CORRESP), responding to SEC comment letter dated September 23, 2016, regarding Form 8-K dated July 22, 2016 (File No. 001-03932). October 4, 2016. https://www.sec.gov/Archives/edgar/data/0000106640/000119312516730214/filename1.htm.