This post builds on my previous one, “Impairment and Amortization: Where Transfer Pricing Analysis Meets GAAP Income Statement Classification,” assuming the Comparable Profits Method (CPM) is chosen under 1.482-1(c) and focusing on building the comparable set. The purpose of this post is to highlight the distinctions between three related accounting terms that are, in practice, mutually exclusive.

“Operating income” is often seen as a single line below SG&A (XSGA) and above non-operating items. This post highlights the distinction between different measures of operating income and why the distinction matters in transfer pricing analysis:

- “Operating profit” as defined by the 1.482-5 regulations.

- “Operating income,” the income statement subtotal labeled on a comparable’s 10-K (most closely aligned with Compustat’s OIADP, operating income after depreciation and amortization), is the voluntary figure with no codified contents under GAAP.

- “Income from continuing operations,” the GAAP-defined measure of period earnings under ASC 205-20-45-3 (generally Compustat’s IB), is a broader, post-tax figure that incorporates a number of items the 482 definition of operating profit explicitly strips out.

Three measures, all in the same income statement neighborhood, none interchangeable for transfer pricing.

In this post, we discuss the structural disparity among the three definitions, each with different purposes and scopes. The gap is so wide that using data from a financial database without standardization can produce an arm’s length range that reflects measurement noise as much as economic differences in profitability.

The 1.482-5(d) Definition

Operating profit under 1.482-5(d)(4) equals gross profit (GP) minus operating expenses, covering all income from the tested activity but excluding interest, dividends, non-tested income, and unrelated gains/losses. Operating expenses exclude interest (XINT), taxes, and unrelated costs. 1.482-5(c)(3)(ii) defines reliability by linking it to accounting consistency affecting operating profit, and 1.482-5(c)(2)(iv) requires adjustments for differences impacting profits. The definition isolates specific business economics, diverging from GAAP, which targets a different audience.

GAAP Has No Definition of Operating Income

The FASB has never codified a definition of “operating income” or “income from operations” in the ASC. Though the term appears frequently in practice, on income statements, and in financial databases like Compustat’s OIADP, standards remain silent on its contents. ASC 225 allows both single-step and multi-step formats, leaving the choice of which subtotals to present to the filer. SEC Regulation S-X, Rule 5-03, prescribes specific income statement line items but does not mandate an “operating income” subtotal, so its contents depend on the company’s classification decisions.

The “operating income” in a comparable’s 10-K is a voluntary, company-defined figure with no fixed scope, varying across registrants. Some companies include interest income (aggregated within NOPI) in an “other operating income” line above the subtotal; others report it below as non-operating. Equity method earnings appear after income tax and before continuing operations, but SEC interpretations allow registrants to present them above the operating income line if the investee’s operations are “integral” to the business, a choice for the registrant. Gains/losses on long-lived asset sales not qualifying as discontinued must be in income from continuing operations and within the “operating income” subtotal, but presentation varies. Restructuring, impairments, and non-recurring items may be included in operating expenses or reported separately, depending on the registrant.

Schilit, Perler, and Engelhart describe the mechanics of this latitude in some detail, observing that “a company taking a one-time charge to write off inventory or plant and equipment would effectively shift the related expenses… out of the Operating section to the nonoperating section and, as a result, push up operating income” — a description the authors frame as earnings manipulation but resting on the same classification flexibility that produces the comparability variance we are addressing here.

Two comparables can report similar “operating income” but measure different things due to classification judgments rather than economic differences. Fabozzi and Drake observe that the latitude registrants exercise in classification choices “make[s] it more challenging to compare companies and to evaluate trends within a company over time.” That observation, from an equity analyst’s perspective, highlights a comparability issue also seen when building a CPM comparable set, but the 482 measure adds a third reference point that is absent from the financial-analysis literature.

The GAAP Definition: Income from Continuing Operations

The GAAP measure, defined with (relative) specificity as income from continuing operations under ASC 205-20-45-3 (Compustat’s IB, income before extraordinary items), is broader than “operating income.” It appears further down the income statement and includes items the 482 definition excludes, such as interest income/expenses, dividend income, equity earnings, securities gains/losses, and income tax expense, excluding only discontinued operations, which are listed below.

Two recent ASUs have made this measure more inclusive. ASU 2014-08 narrowed the definition of discontinued operations, causing fewer dispositions to qualify and shifting more gains and losses into continuing operations. ASU 2015-01 removed the extraordinary items concept from GAAP, meaning items like disaster losses, litigation settlements, and write-downs, previously below income from continuing operations net of tax, are now included in that measure.

GAAP’s measure of period earnings differs from the 1.482-5 definition of operating profit, making ‘income from continuing operations’ a substantially different measure. Using it as a substitute in CPM analysis introduces a larger measurement error than using the 10-K “operating income” subtotal.

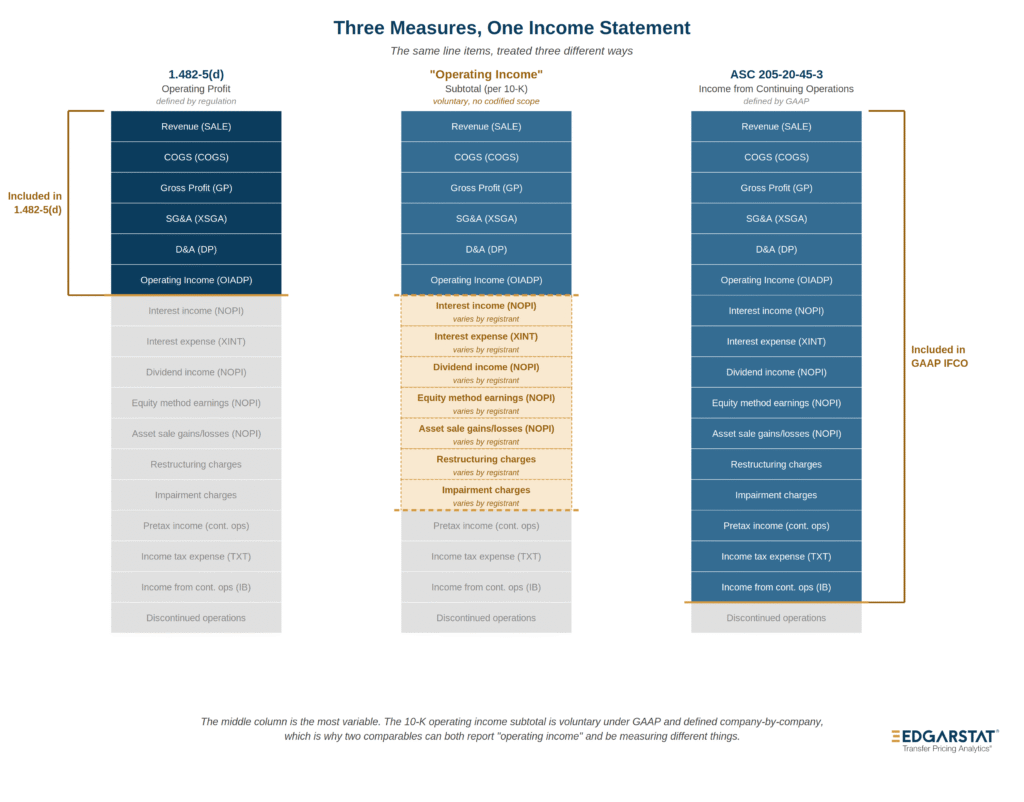

Three Measures Side by Side

The disparities across the three measures aren’t always intuitive when described in prose. The visual below maps how each of the most common income statement items is treated under each framework, with the relevant Compustat mnemonics shown in parentheses for ease of cross-reference against the database fields.

The middle column contains most ‘varies by registrant’ entries and is what analyses use when reported data is pulled directly from a database without adjustment. The outer columns are defined frameworks (one regulatory, one under GAAP), though there are some differences. The middle column lacks a strict framework, causing comparability issues within a typical comparable set.

Some items in the visual merit closer look due to their substantial magnitudes and unclear structural differences from a single line of text.

Amortization of Acquired Intangibles

Amortization of acquired intangibles (AM) appears in operating profit under all three frameworks. According to 1.482-5(d)(3), operating expenses cover “a reasonable allowance for depreciation and amortization,” so amortization is included in operating profit; this applies to the 10-K subtotal and GAAP income from continuing operations. The issue is not a definitional mismatch but a comparability problem within the set caused by ASC 805 (business combinations).

A comparable company that made a large acquisition during or before the tested period will have substantial amortization of acquired intangibles, which flows through operating expenses and depresses OMAD. In contrast, a similar company that grew organically won’t have that expense, even if both perform similarly at similar gross margins; their OMADs may differ due to unrelated factors. The acquisition history affects reported operating profit independently of actual economic performance, leading to significant discrepancies, especially when large purchase price allocations can shift OMAD by hundreds of basis points.

Impairment Charges

Impairments like goodwill, indefinite-lived intangible assets, and long-lived assets distort an arm’s length range when unexamined. Recognized in income from continuing operations, they affect reported “operating income” and ASC 205-20-45-3 income. The key question for transfer pricing analysis is whether the impairment relates to ongoing business, which it usually does not, as these charges reflect reassessments of historical acquisition values rather than current performance.

Goodwill impairments can reach hundreds of millions, turning profitable comparables into significant losses not related to core operations but due to declines in fair value at the reporting unit level under ASC 350-20. Such impairments do not reflect the arm’s length return from usual business activities, which CPM analysis aims to measure. Including a $400 million impairment in “operating income” impacts the entire arm’s length range, and similar effects occur with impairments of long-lived assets and indefinite-lived intangibles.

Restructuring Charges

Restructuring charges, like impairments, appear in the 10-K “operating income” and GAAP income from continuing operations. Under 1.482-5, their treatment depends on whether they relate to the tested business. A benchmarking set with some comparables showing large restructuring charges and others none will reflect corporate restructuring activity, not operating profitability.

The Extraordinary Items Residue

Section 1.482-5(d)(4) still mentions “extraordinary gains and losses” unrelated to the continued operations of the tested party, but this language predates ASU 2015-01, which removed the extraordinary items concept from GAAP. Now, litigation settlements, disaster losses, and write-downs, once classified as extraordinary, are included in the “operating income” and income from continuing operations without special labels. The exclusion principle in 1.482-5(d)(4) likely remains, focusing on the substance of items rather than the outdated GAAP category. However, the regulations haven’t been updated, leading to potential disagreements between practitioners and examiners over interpretation.

The Three-Way Disparity’s Impact on the Arm’s Length Range

The disparities described above introduce inconsistencies in the comparable set that aren’t always visible and tend to propagate. If one comparable’s “operating income” includes $4 million of interest income (blended into an “other operating income” line) while another excludes it (reported as a non-operating item), the PLIs are measured on different bases before the 1.482-5(d) issue. With ten or fifteen comparables, each with its own classification choices on earnings, gains, charges, impairments, amortization, and stock-based compensation, the arm’s length range reflects classification noise as much as economic differences.

An examiner or competent authority can challenge an inconsistent set under 1.482-1(c) by arguing that a different or properly adjusted method would yield more reliable results.

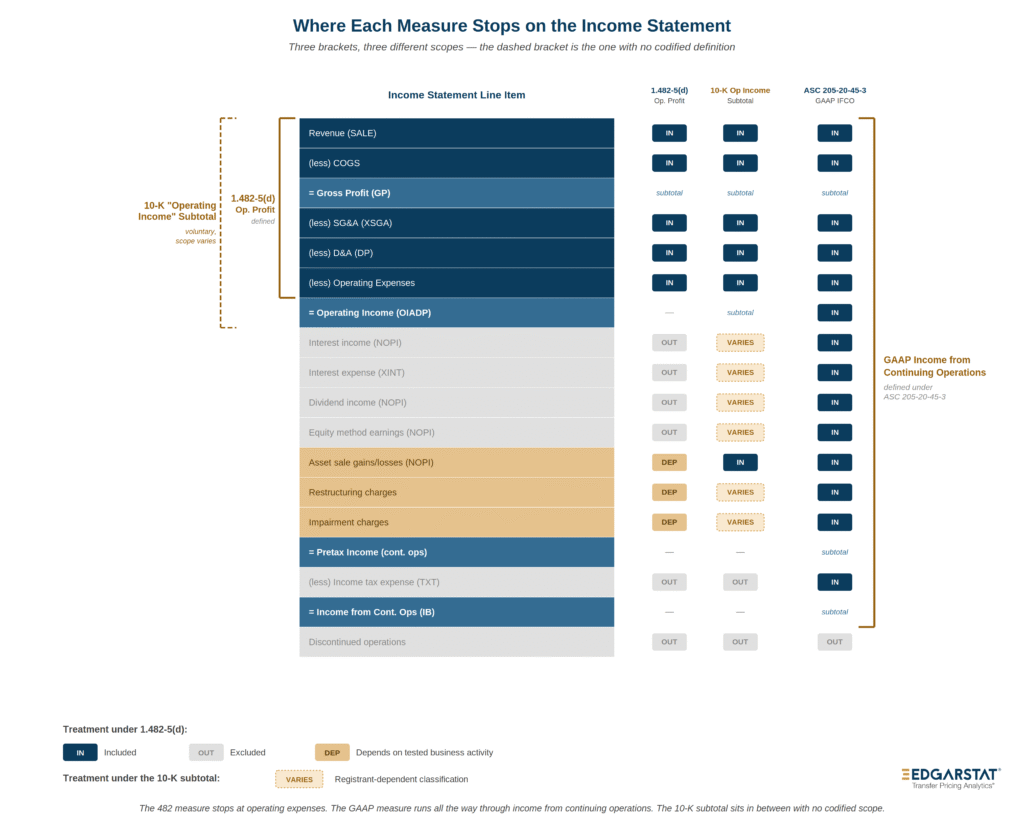

The visual below traces each point on the income statement, showing where each measure ends and which line items it encompasses.

Proper Standardization (Mostly) Resolves the Three-Way Disparity

The disparities described in the preceding sections are built into the income statement data used in a CPM analysis whenever comparable financials are pulled directly from a public source without further adjustment. The middle column of the diagram (the “operating income” subtotal as reported on the 10-K) is the column many databases default to, and the variability within that column across registrants produces an arm’s length range that reflects classification noise alongside economic differences in profitability. The disparity between that middle column and either of the outer two (the 1.482-5(d) definition and the GAAP IFCO measure under ASC 205-20-45-3) is also baked into the data, and resolving it on a per-comparable, after-the-fact basis requires substantial analytical work.

EdgarStat

EdgarStat’s database of publicly listed company financials provides multi-year financial and XBRL data, standardized for transfer pricing analysis. It addresses variability and ensures PLI inputs are measured uniformly, supporting a reliable arm’s length range per 1.482-5(c)(3)(ii).

Why a Single Source of Standardized Data Matters

A CPM analysis’s reliability depends on the internal consistency of the comparable set. A database sourcing financial data from multiple, differently standardized and classified sources can create “operating income” fields that aren’t measured uniformly across companies. This inconsistency isn’t visible in the current output: Company A’s operating income may have been standardized with one methodology including equity earnings, while Company B’s used a different method excluding them. The arm’s length range then reflects methodological differences, not true economic differences. Using a single standardization methodology on one data source reduces this noise.

Public Company Data Is the Most Reliable Input

Public company financials filed with the SEC, audited by PCAOB-registered auditors, and XBRL tagged, offer transparency and standardization not found in private company data. Private financials are often unaudited or subject to lesser assurance standards, such as compilations and reviews, and they lack mandatory disclosures such as disaggregated revenue, non-operating income, or related-party transactions, making them less reliable for comparison. Combining public and private data introduces reliability issues, as mixed sources do not provide a consistent measure of arm’s length profitability.

A Note on Evolving GAAP — ASU 2024-03

ASU 2024-03 applies to public entities for annual periods after December 15, 2026, and interim periods after December 15, 2027. It mandates more granular disaggregation of significant income statement expenses (DISE), improving the comparability of comparable company operating expenses per 1.482-5(d)(3). I look forward to discussing this standard further once SEC filings include it.

Wrapping Up

The three measures of operating profitability discussed in this post — (1.482-5(d) operating profit, the voluntary “operating income” subtotal on a 10-K, and GAAP income from continuing operations under ASC 205-20-45-3) — are often conflated, but differ significantly in their composition. The 1.482-5 measure is narrowly defined for transfer pricing; the 10-K subtotal is voluntary and varies across registrants; and GAAP IFCO is the broadest and most different from 1.482-5, risking inconsistency in the arm’s length range if employed.

Primary Source Reference List

| Source | Citation |

|---|---|

| IRC § 482 | 26 U.S.C. § 482 |

| CPM Regulations | Treas. Reg. § 1.482-5(a)–(e) |

| Best Method Rule | Treas. Reg. § 1.482-1(c) |

| Comparability Standards | Treas. Reg. § 1.482-1(d) |

| GAAP — Comprehensive Income | ASC 220-10-45-7, 220-10-45-8 |

| GAAP — Income Statement | ASC 225-20 |

| GAAP — Discontinued Operations | ASC 205-20-45-3 |

| GAAP — Long-Lived Asset Disposals | ASC 360-10-45-5 |

| GAAP — Goodwill Impairment | ASC 350-20 |

| GAAP — Intangible Asset Impairment | ASC 350-30 |

| GAAP — Long-Lived Asset Impairment | ASC 360-10-35 |

| GAAP — Business Combinations | ASC 805 |

| Extraordinary Items Eliminated | ASU 2015-01 |

| Discontinued Operations Narrowed | ASU 2014-08 |

| Expense Disaggregation | ASU 2024-03 |

| SEC Income Statement Requirements | Regulation S-X, Rule 5-03 |

| Standardized Public Company Financials | EdgarStat (edgarstat.com) |

| Standardized Reporting Taxonomy | XBRL US / FASB US GAAP Financial Reporting Taxonomy |

Additional References

Fabozzi, Frank J., and Pamela Peterson Drake. Analysis of Financial Statements. 3rd ed. Hoboken, NJ: John Wiley & Sons, 2012.

Schilit, Howard M., Jeremy Perler, and Yoni Engelhart. Financial Shenanigans: How to Detect Accounting Gimmicks and Fraud in Financial Reports. 4th ed. New York: McGraw-Hill Education, 2018.