Inventory markdown disclosure in U.S. public filings runs on two regulatory tracks. GAAP under ASC 330 sets a narrow trigger that applies only to a defined subset of markdown activity. The SEC overlay under Regulation S-K is where the substantive markdown discussion appears in most 10-K filings. The two layers don’t align cleanly, and the §482 analyst has to read both of them.

The GAAP Layer: ASC 330

The central disclosure provision for inventory markdowns is ASC 330-10-50-2, which provides that “substantial and unusual losses that result from the subsequent measurement of inventory … should be disclosed in the financial statements.” Both prongs must be present. A material but routine markdown doesn’t satisfy the standard, no matter how large the dollar effect on COGS. Seasonal reductions in apparel inventories and end-of-cycle clearance at fashion retailers flow through COGS via the lower-of-cost-or-NRV reserve, with no separate disclosure required. A markdown clears the threshold when it’s both large in dollars and outside the ordinary course of business. Pandemic-driven write-downs and brand or product-line exits are examples of such events. The $271.9M Q1 FY2020 reserve recorded by one major off-price retailer in response to COVID-19 store closures illustrates both prongs within a single event.

The Interim Reporting Constraint: ASC 270

ASC 270-10-45-6 governs the timing of recognition. The filer recognizes a market-value decline in the interim period when it occurs, and cannot defer recognition to year-end unless the decline is reasonably expected to reverse before the fiscal year closes. That requirement explains why the $271.9M reserve appeared in Q1 FY2020 rather than later. Once recognized in an interim period, assuming the loss meets the substantial-and-unusual standard, the ASC 330-10-50-2 named disclosure applies at the 10-Q stage and persists into the annual 10-K.

The SEC Overlay

Regulation S-K Item 303 governs Management’s Discussion and Analysis (MD&A). Item 303(b)(2)(i) requires discussion of any unusual or infrequent events or transactions, and any significant economic changes, that materially affected reported results. A markdown event that moved gross margin by hundreds of basis points satisfies that requirement even when the underlying loss wouldn’t clear the substantial-and-unusual standard of ASC 330-10-50-2. Item 303(b)(2)(ii) extends the disclosure to known trends and uncertainties. Once a building markdown problem becomes reasonably foreseeable, the filer must discuss it prospectively.

Practical Synthesis

In practice, the disclosure outcomes look like this:

| Situation | Disclosure | Location |

|---|---|---|

| Routine seasonal markdowns | Nothing specific; embedded in COGS | — |

| Substantial and unusual loss event | Named, quantified disclosure | Financial statements (ASC 330-10-50-2) and MD&A |

| Material impact on gross margin in a period | Discussion of drivers | MD&A under Reg S-K Item 303 |

A Fifteen-Filer Case Study: Inventory Markdown Disclosure Across an Apparel Retail Comparable Set, FY2018 through FY2024

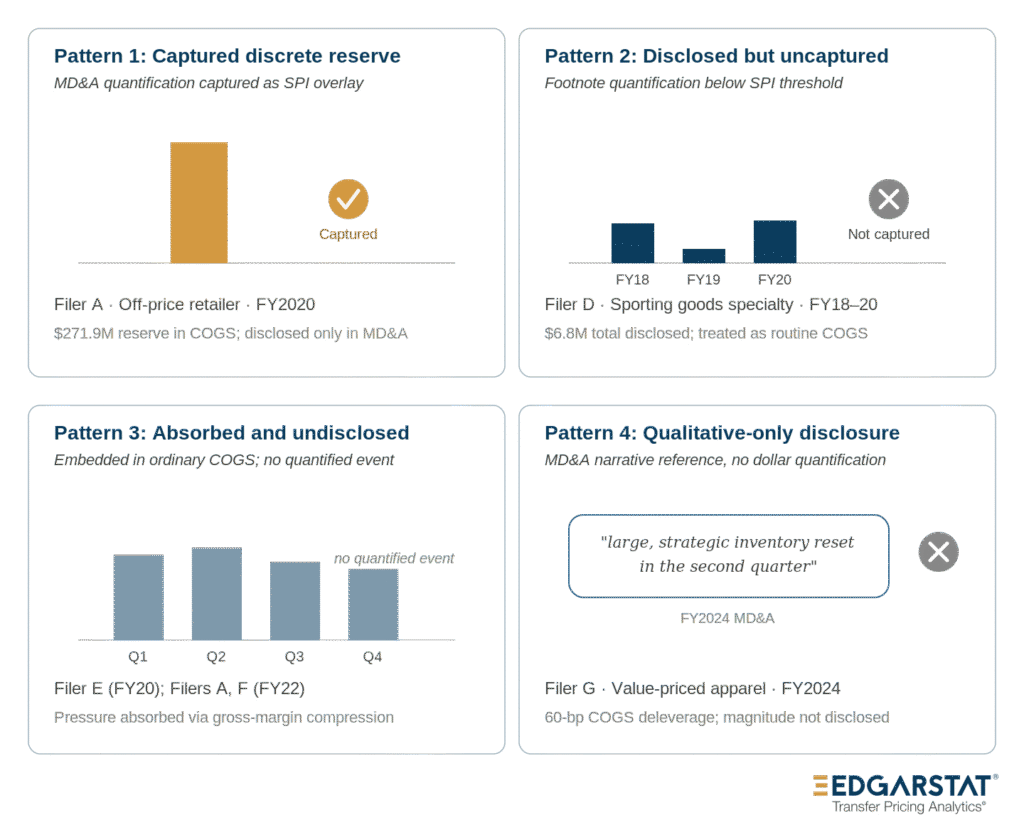

We reconciled disclosed inventory items in 10-K and 10-Q filings against Compustat’s Special Items (SPI) capture across a fifteen-filer apparel retail comparable set covering FY2018 through FY2024. The reconciliation produces four distinct disclosure patterns. Eight filers serve as exemplars below under anonymized designations (Filer A through Filer H), and each is explained in turn. The remaining seven filers either show no notable inventory disclosure events during the window or exhibit smaller-magnitude instances of the four patterns.

| Pattern | Filers (FY) | Disclosure form | Compustat treatment |

|---|---|---|---|

| 1: Captured discrete reserve | A, B, C (FY2020); H (FY2023) | MD&A-quantified | Analyst SPI overlay applied |

| 2: Disclosed but uncaptured | D (FY2018, FY2019, FY2020) | Footnote-quantified, small magnitude | Treated as routine COGS |

| 3: Absorbed and undisclosed | E (FY2020); A, F (FY2022) | None | Recorded as ordinary gross-margin compression |

| 4: Qualitative-only | G (FY2024) | MD&A qualitative only | Not capturable |

Pattern 1: The Captured Discrete-Reserve Cohort

Three filers booked discrete Q1 FY2020 inventory reserves in cost of sales, and Compustat captured each as an analyst overlay. Filer A, an off-price retailer, recognized a $271.9M markdown reserve disclosed in the MD&A liquidity discussion with no income statement caption. Filer B, a legacy multi-brand specialty retailer, recognized $235M in Q1 seasonal stranded inventory together with impaired garment and fabric commitments, also disclosed in MD&A. Filer C, a children’s specialty retailer, recognized a $63.2M COVID inventory provision that Compustat captured at a partial-estimated amount. Filer H, a casual apparel specialty retailer, illustrates the same pattern outside the COVID window: an $11M international inventory writedown recognized in FY2023, disclosed in MD&A, and captured by Compustat as an analyst overlay. The four cases share two features: the disclosure appears in MD&A rather than in the footnotes, and the event is absent from the face of the income statement. Compustat applied an analyst overlay in each case because the disclosed magnitude and the surrounding narrative provided the structured-data layer with enough information to derive a markdown figure. This is the empirical realization of the ASC 330-10-50-2 threshold working alongside Reg S-K Item 303(b)(2)(i).

Pattern 2: The Disclosed but Uncaptured

Filer D, a sporting goods specialty retailer, discloses four distinct inventory items across FY2018 through FY2020 totaling $6.8M. The items consist of a $1.9M inventory step-up recorded under purchase accounting in FY2018, a $0.9M Team Division inventory reserve also recorded in FY2018 and described in MD&A as a one-time charge, $1M of step-up amortization in FY2019, and a $3M COVID lower-of-cost-or-market reserve in FY2020. Compustat treats all four as routine COGS activity. The filer-side disclosure exists and includes a footnote in each case, but the dollar amounts don’t clear the magnitude threshold below which Compustat declines to apply an SPI overlay. For a practitioner relying on the structured-data layer rather than reading each comparable’s 10-K, this pattern produces a systematic understatement of comparable-side SPI relative to the disclosed nonrecurring activity in the underlying filings.

Pattern 3: The Absorbed and Undisclosed

Three filer-year combinations illustrate this pattern. Filer E, a women’s specialty retailer operating against going-concern doubt in FY2020, absorbed COVID inventory pressure through ongoing markdowns and made no event-level disclosure. Neither the income statement nor the MD&A discussion quantifies a discrete markdown action. Filer A, the same off-price retailer that disclosed $271.9M in FY2020, absorbed FY2022 supply-chain bloat through reported gross margin, with inventory growing $424M year-over-year. No separate markdown disclosure appeared in either the financial statements or MD&A. Filer F, a men’s big-and-tall specialty retailer, followed the same pattern with $24.5M of FY2022 inventory growth absorbed similarly. The within-filer observation across Filer A is independently useful. The same company chose discrete recognition in FY2020 and silent absorption in FY2022, indicating that the disclosure decision is context-dependent and not a fixed characteristic of the filer.

Pattern 4: The Qualitative-Only Disclosure

Filer G, a value-priced apparel retailer, discloses in its FY2024 MD&A that COGS deleveraged by 60 basis points because of “a large, strategic inventory reset in the second quarter,” without quantifying the markdown amount. Compustat cannot apply an SPI overlay in the absence of a calculable dollar figure. The reset itself is real, and the qualitative disclosure satisfies Reg S-K Item 303(b)(2)(i), but the structured-data layer has no usable hook to capture it. A practitioner reading the Compustat SPI value alone will see a clean comparable; the same practitioner reading the MD&A will see a substantial inventory action absorbed into the cost-of-sales line.

Takeaways From the Data

Across the four patterns, the disclosure asymmetry takes concrete form. The FY2020 COVID shock created a near-experimental setting: a single exogenous economic event produced widely varying disclosure choices across the comparable set, and those choices correlated with each filer’s pre-shock financial position. The FY2022 supply-chain cohort gives us the same observation under a less severe shock, with a less dramatic disclosure spread. Filer A’s behavior across time matters most. The same company made two different disclosure choices three years apart, driven by changes in the macro environment rather than any (disclosed) shift in internal policy. For a comparability analysis built solely on Compustat-reported SPI, the four patterns together imply systematic measurement error in any comparability framework that relies on disclosed inventory items. The implications section below develops the source of that error.

Implications for Transfer Pricing Analysis

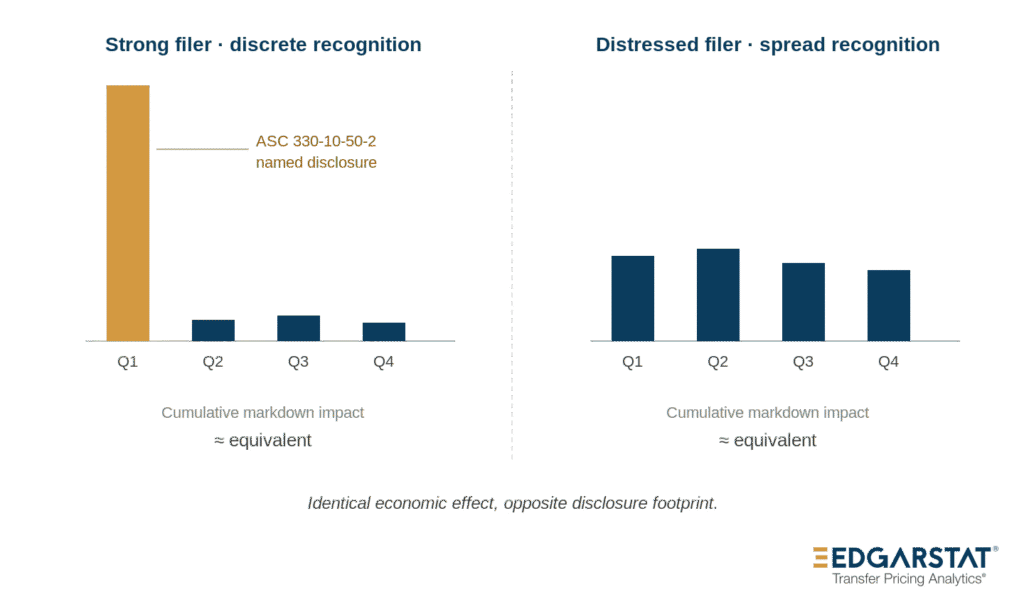

This framework has direct consequences for CPM comparability analysis under §482. When a comparable’s 10-K shows no quantified inventory write-down, the proper inference is narrow: the markdowns either failed to satisfy the substantial-and-unusual threshold of ASC 330-10-50-2, or the filer chose not to quantify them in MD&A. Either way, the gross-margin compression in reported results already reflects the economic impact of any unrecognized markdown activity. For a retailer whose FY2020 gross margin compressed relative to historical norms, the markdown activity is fully reflected in the reported operating margin, even when no discrete write-down figure appears in the notes.

The asymmetry also runs in one direction. Companies in strong financial positions have the latitude to take large, discrete reserves and reset their inventory baselines. Filer A’s $271.9M Q1 FY2020 reserve reflects that approach: sufficient liquidity to absorb the immediate earnings impact, and a decision to enter the recovery period with a clean inventory base. Companies under financial distress face the opposite incentive. Spreading markdown pressure across multiple quarters through ongoing reserve adjustments produces less severe quarterly earnings impact than concentrated recognition, even when the cumulative economic effect is comparable. Filer E, the specialty apparel retailer operating under going-concern doubt during the same FY2020 window, followed that pattern precisely. Any keyword-driven 10-K screen for inventory write-downs will over-represent disclosed events from financially stronger comparables and under-represent the diffuse markdown activity of distressed peers.

The Inherent Comparability Problem

The takeaway is that the disclosure regime is vague enough to make any clean comparability analysis hard to defend. Filer discretion enters at multiple points. ASC 330-10-50-2’s “substantial and unusual” trigger turns on judgment about what counts as substantial and what counts as unusual, and Reg S-K Item 303(b)(2)(i) demands a parallel exercise of discretion in identifying “unusual or infrequent events.” Beyond the triggers, the standards leave the choice of reporting vehicle, whether a face income statement caption, a financial-statement footnote, or an MD&A narrative, almost entirely to the filer. The same economic event, occurring contemporaneously across a set of comparable companies, can produce four distinct reporting outcomes across the set without any filer violating a disclosure rule. The case study above documents this: the FY2020 COVID shock produced discrete reserves captured for some filers, footnoted-but-uncaptured items for another, silent absorption for yet others, and a purely qualitative reference for a fourth. None of these reporting choices is improper under the standards as written.

Heterogeneity in inventory markdown disclosures introduces measurement error that no amount of additional data collection or more sophisticated screening can eliminate. The error is built into the regulatory framework that produces the comparables’ financials. The vagueness in the disclosure regime is a legitimate feature whose measurement differences must be accounted for in comparability analysis.