Intercompany financing has attracted numerous challenges from government agencies in recent years. On May 12, the General Court of the European Union ruled in favor of the European Commission’s decision that a favorable Luxembourg ruling with respect to an intercompany loan for Engie conveyed an illegal tax advantage. While this ruling focused on legal issues, we will discuss whether the pricing of the intercompany loan was at arm’s length. Perrigo is facing tax challenges from the Irish, Israeli and US tax authorities. The IRS challenge to a $7.5 billion intercompany loan focuses on its pricing.

Engie State Aid Case

Engie (formerly GDF Suez) is a French energy multinational operating in 70 nations with revenues exceeding €66 billion ($80 bil.) in 2016. GSTM is its Luxembourg financing affiliate. Engie acquired a Luxembourg supply affiliate for approximately $750 million financed in part by an intercompany loan that was approximately $650 million.

The European decision noted that the intercompany loan was signed on October 30, 2009 and was a 15- year fixed-interest rate loan. The agreement also specified a 2% loan margin. While the borrowing affiliate deducted its intercompany expenses in full, GSTM’s taxable income was limited to the loan margin. The European Commission did not specify the intercompany interest rate, but it is reasonable to assume that this interest rate was the sum of the corresponding government bond rate and the loan margin.

On October 30, 2009 the interest rate on 10-year government bonds was 3.41% and the interest rate on 20-year government bonds was 4.19%. While the US government does not issue 15-year bonds, it is reasonable to assume that the corresponding government bond rate was 3.8% since the term of the intercompany loan was 15 years. As such, the intercompany interest rate was 5.8%.

Table 1 presents the annual interest rate for a $650 million loan under alternative interest rates. If the interest rate = 5.8%, then interest expenses = $37.7 million per year. Using the 3.8% government bond (GB) rate, interest expenses would be $24.7 million per year. This lower amount is the amount of taxable income that has been exempted by this Luxembourg ruling, as the financing affiliate is only being taxed on the $13 million difference.

Table 1: Perrigo Intercompany Interest Expenses under Alternative Credit Spreads (In Millions)

| Percentage | Interest Expense | |

| GB Rate | 3.8% | $24.7 |

| Loan Margin | 2.0% | $13.0 |

| Interest Rate | 5.8% | $37.7 |

The European Commission ruling was based on this exemption of taxable income and not on whether the intercompany interest rate was arm’s length. A strong defense for the arm’s length nature exists even if the borrowing affiliate’s was set at the group credit rating, which was BBB for Engie at the time of this intercompany loan. Interest rate on long-term US dollar denominated corporate debt with BBB credit ratings at the time was 6.2%, which implies that the appropriate credit spread was 2%.

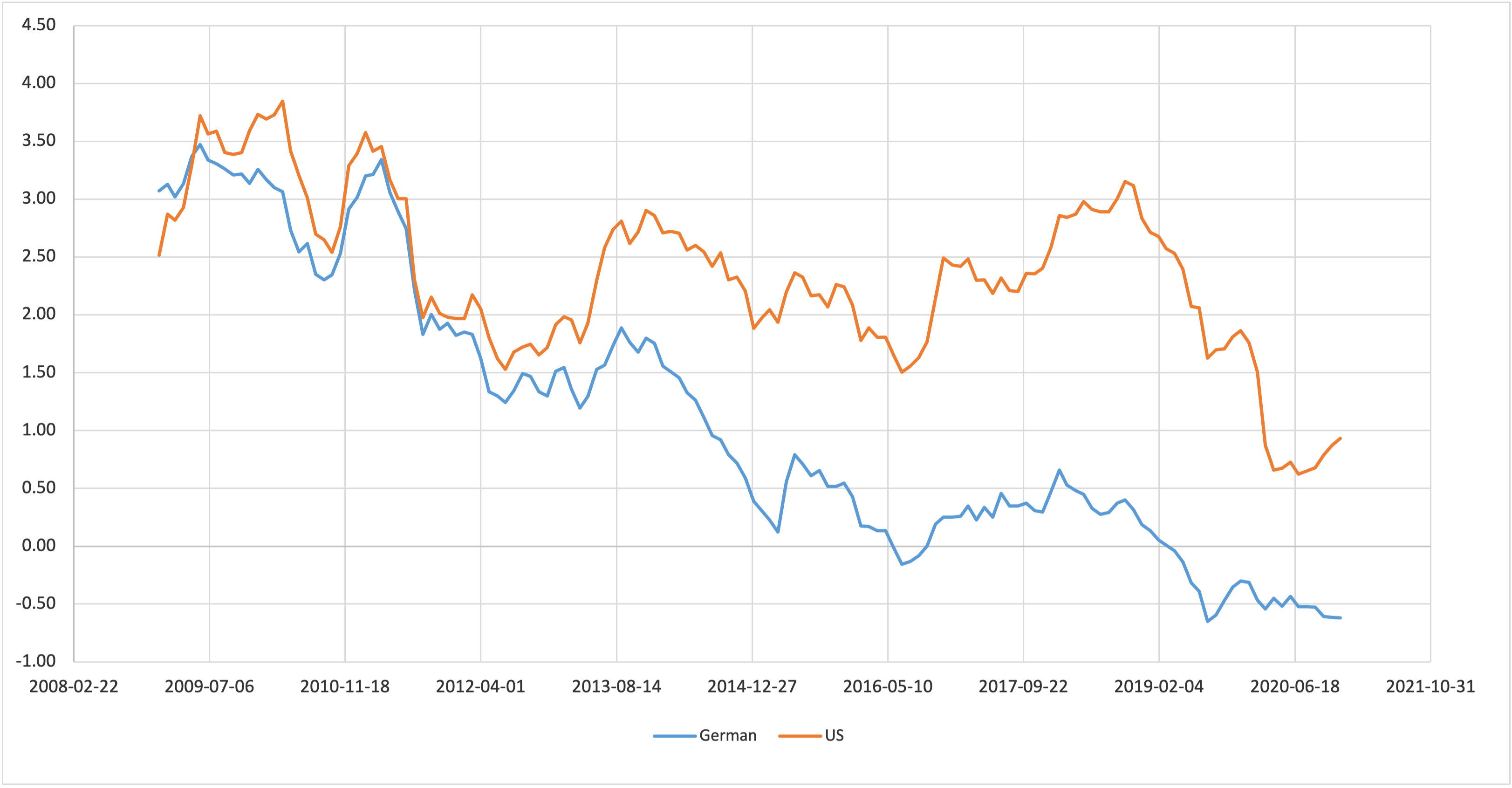

Engie secured a 1.5% interest rate on an €850 million ($1.037 billion) loan as of November 19, 2020. This very low third-party interest rate, however, does not imply that the 5.8% interest rate was above the arm’s length. As the following chart shows, interest rates in late 2020 were much lower than interest rates in late 2009. It also shows that interest rates on German government bonds were lower than interest rates on US government bonds. If the interest rate on the corresponding government bond is less than negative 0.5%, then the credit spread exceeds 2%.

Ten year government bonds in Germany and the US: January 2009 to December 2020

An IRS Challenge to Perrigo’s Intercompany Financing

Perrigo’s 10-K filing for fiscal year ended December 31, 2020 discussed various challenges from the IRS including a dispute on what should represent an arm’s length interest rate on a $7.5 billion intercompany loan that was incurred in connection with the merger when Perrigo purchased Elan in late 2013 for approximately $8.5 billion.

The IRS has proposed a reduction in the intercompany interest rate near 4% where its position is that this interest rate should be based on 130% of the Applicable Federal Rate. While the proposed adjustments in the original IRS 30-day letter extended only through June 30, 2015, the 10-K filing notes that this issue extends to the end of 2018.

Let’s assume a 5-year intercompany loan with a fixed interest rate of 6.25% was extended on January 9, 2014. On that date, the interest rate on 5-year government bonds was 1.75%, so the credit spread implied by the intercompany loan would be 4.5%.

The midterm Applicable Federal Rate for January 2014 was 1.74%. The IRS position is therefore that the interest rate should be only 2.25%, which is consistent with a credit spread of only 0.5%. Table 2 presents these two positions as well as two intermediate positions.

The intercompany policy results in $468.75 million per year in interest deductions. The IRS position would lower these deductions to only $168.75 million per year. The IRS position, however, is not well founded, as it is consistent with a AAA credit rating, even though the group credit rating for Perrigo was BBB. Credit spreads for BBB rate corporate debt would tend to be near 1.5%, which would imply that the parent would have to pay an interest rate of 3.25%.

The taxpayer’s position is reasonable if it can make a credible case that the borrowing affiliate’s credit spread should be B+. If the appropriate credit rating were BB, the credit spread would be 3%. Under this interpretation, the appropriate interest rate would be 4.75%, implying interest deductions equal to $356.25 million per year.

Table 2: Perrigo intercompany interest expenses under alternative credit spreads

| AAA Rating | BBB Rating | BB Rating | B+ Rating | |

| Credit spread | 0.5% | 1.5% | 3.0% | 4.5% |

| Interest rate | 2.25% | 3.25% | 4.75% | 6.25% |

| Interest expense | $168.75 | $243.75 | $356.25 | $468.75 |

The issue of what represents an appropriate credit spread has been the subject of considerable controversy including litigations in Australia and Canada. The OECD and the United Nations have also commented on this issue, noting the implicit support standards that we discussed in the GE Capital Canada and Chevron Australia litigations.

Let’s imagine that Perrigo has commissioned an analysis of the standalone credit rating for the US borrowing affiliate that supports its 4.5% credit spread. Would the IRS simply accept this analysis or would it adopt this implicit support doctrine? If the IRS adopted that strong support position that the Canadian Revenue Agency argued in the GE Capital Canada litigation, the lowest interest rate it could argue as being arm’s length would be 3.25% and not the 2.25% rate representing 130% of the Applicable Federal Rate.

It must be noted that the Canadian courts rejected the strong support position. The Australian Tax Office did not even argue this strong support position in its successful litigation of this issue in the Chevron Australia litigation. If similar logic prevails in the Perrigo case, an intermediate result may prevail.

References