Separate-entity state tax base exposure to international transfer pricing if federal enforcement priorities shift from § 482 to attribution, and why many states already possess the statutory authority to respond without new legislation.

“Plurality must never be posited without necessity.” — William of Ockham

Background and abstract

This blog entry was inspired by a Multistate Tax Commission (MTC) Briefing Book (“the book”) published March 13, 2026, entitled “Changes in Federal Taxation of Multinational Corporate Groups: How these changes will affect state corporate taxes and state policy choices.”

I discussed this document briefly during the recent transfer pricing panel at the SEATA 2026 conference. Given its implications, the book warrants a closer look at the problems it identifies and the prescriptions it offers.

The book, in my view, correctly characterizes the base erosion risks faced by separate-entity and water’s-edge reporting states in a federal regulatory environment expected to concentrate compliance on codified attribution regimes (GILTI/NCTI) rather than on costly, slow-moving transfer pricing disputes. A shift of this kind would leave the federal side of a decades-old informal agreement between the federal government and the states unperformed, exposing state corporate tax bases to erosion from international income shifting that the federal government would no longer be keen to pursue.

The book’s prescriptions are primarily legislative in nature: states may adopt mandatory worldwide combined reporting (WWCR) or modify statutes to conform to the § 951A inclusion; the book separately recommends against conforming to the § 250 special deductions.

I argue in this entry that many states already possess the statutory authority to bridge the regulatory gap anticipated in the book. That authority supports adjustments to the domestic entity’s operating income, tested against comparable-company benchmarks, avoiding what the book identifies as burdensome intangible valuations that make federal transfer pricing enforcement costly. If the MTC’s forecast is realized, the state tax base erosion in many states can be remedied through enforcement of existing statutes, with no change to the law required.

The MTC forecast

The federal taxation of multinational corporate groups has over time shifted through three tax acts, from a transfer pricing system to an attribution-based system. Section 482, enacted in substance as § 45 of the Revenue Act of 1928, gave the Commissioner authority to reallocate income and deductions among commonly controlled entities so as to reflect arm’s-length results. The 2017 Tax Cuts and Jobs Act (TCJA), as part of a transition from a worldwide to a hybrid-territorial system, added § 951A (“the inclusion”), which attributed a measure of controlled foreign corporation (CFC) income, called global intangible low-taxed income (GILTI), to the U.S. shareholder in the year the income was earned. The 2025 legislation (OBBBA) carried the approach further, renaming the inclusion Net CFC Tested Income (NCTI), removing the qualified business asset investment (QBAI) reduction, and revising the § 250 deduction (50% to 40%) and the foreign tax credit (FTC) (80% to 90%), effective for tax years beginning after December 31, 2025.

The MTC, in its March 2026 staff briefing book prepared for member states, draws a prediction from this history. As federal compliance shifts toward attribution, the MTC expects the IRS to reduce its transfer pricing enforcement and to concentrate its resources on the new attribution regime.

That prediction is contestable; § 482 remains in force, and the Large Business and International (LB&I) division continues to litigate substantial transfer pricing cases. Whether federal enforcement contracts as the MTC anticipates is a question of resource allocation that cannot be settled here. The analysis below addresses only the structural reliance that separate-entity reporting states have placed on federal enforcement.

A state that neither conforms to the federal inclusion of NCTI nor combines the income of foreign affiliates has, whether by policy or by inertia, delegated the protection of its domestic base against international income shifting to federal audit authorities. If those rules are enforced less vigorously, the state’s exposure increases, and no party other than the state itself is positioned to address it.

To address this exposure, the book presents two policy alternatives: 1) state conformity to the federal inclusion of NCTI and 2) mandatory WWCR. Both proposals have a contentious political history and would require new legislation in many states, which abandoned mandatory WWCR in the 1980s under pressure from foreign trading partners and the federal government. State conformity to the inclusion has drawn organized opposition where it has been proposed, including objections submitted to New Mexico’s governor regarding Senate Bill 151, as the book describes.

This blog entry explores a third path that the book addresses only briefly: most of the separate-entity states surveyed below already possess codified authority to adjust related party transactions, whether through direct conformity to § 482 or through an arm’s-length analog, so the erosion the MTC describes can be addressed in those states by administering statutes already in force.

Conformity and the accommodation

Most states calculate net income by reference to federal taxable income (FTI), beginning with the amount reported on Line 28 or Line 30 of federal Form 1120 and applying enumerated additions and subtractions. In separate-entity states, FTI is computed on a separate-entity basis, so the reported results of § 482 transactions are already built into the income of each entity that files a state return.

When the U.S. Supreme Court upheld state authority to require WWCR in Container Corp. v. Franchise Tax Board, 463 U.S. 159 (1983), and again in Barclays Bank PLC v. Franchise Tax Board, 512 U.S. 298 (1994), foreign trading partners and the federal government objected. A working group convened by the Treasury Secretary produced an informal accommodation under which the states agreed to abandon mandatory WWCR in exchange for a federal commitment to enforce the transfer pricing regulations for international related-party transactions. Separate-entity states’ current dependence on federal enforcement of international transfer pricing is a consequence of that accommodation, and the MTC’s forecast, if correct, would mean that the federal side of the accommodation is no longer being performed as understood.

The tax base exposure is concentrated among states that report on a separate-entity basis or a water’s-edge unitary basis. A state that requires water’s-edge unitary combined reporting already eliminates the effect of intercompany transactions among the members of its combined group, so the domestic shifting problem is addressed within the combined return, although water’s-edge combination leaves the international component, the subject of this article, unaddressed. A state that conforms (in whole or in part) to the federal inclusion of NCTI captures a portion of foreign earnings. A separate-entity state that does neither is left with its own statutes governing related-party transactions as its protection against tax base erosion through international transfer pricing.

The § 951A inclusion is not a dividend

The mechanism by which foreign earnings escape a separate-entity state’s base begins with a characterization question that the MTC treats as central and that recent authority has settled. The § 951A amount is an inclusion, an amount taken into the U.S. shareholder’s gross income in the year the CFC earns it, rather than a distribution of accumulated earnings. The Internal Revenue Code (IRC) does not treat the inclusion as a dividend. In Moore v. United States, 602 U.S. 572 (2024), the Supreme Court described subpart F and its successors as attributing the income of CFCs to their American shareholders and taxing the shareholders on that income in a passthrough manner. The MTC observes that many states have nonetheless characterized the inclusion as a “deemed dividend,” a term the IRC does not use in this setting, and it identifies that characterization as an error.

The federal return complicates the characterization through its form nomenclature. The inclusion is computed on Form 8992 and flows to Schedule C of Form 1120, entitled “Dividends, Inclusions, and Special Deductions,” and the Schedule C total flows to Form 1120, page 1, Line 4, captioned “Dividends and Inclusions.” The inclusion therefore appears on the schedule that reports dividends and on a page-one line labeled dividends, although the statute treats NCTI as an income inclusion rather than a dividend distribution. This form placement allows a state dividend deduction to exclude the inclusion from income, as described below.

Two stages of state tax base erosion

A separate-entity or nonconforming state excludes shifted foreign earnings from its base at two stages:

At inclusion

The state may decouple from § 951A by statute, subtracting the inclusion in the computation of state taxable income. Three separate-entity reporting states illustrate this approach, divided between two techniques that achieve the same result: Florida and Virginia limit the subtraction to the net amount that survived the federal computation, while North Carolina subtracts the full inclusion and separately restores the § 250 deduction.

Florida subtracts the inclusion under § 220.13(1)(b) of the Florida Statutes, which removes amounts included in FTI under §§ 78, 951, and 951A, allowed only to the extent those amounts were not deductible in determining FTI, with a corresponding addition of the expenses attributable to the subtracted amount. The inclusion is therefore removed from the Florida base to the extent it entered that base, and under § 220.13(1)(b)6 the apportionment factors related to the excluded income are removed from both the numerator and the denominator of the receipts factor, so no factor representation reflects the amount.

Virginia applies the same technique through its subpart F subtraction. Virginia Code § 58.1-402(C)(7), which subtracts income included under § 951, was expanded to address amounts included in FTI under § 951A, and the subtraction is allowed only to the extent the amount was included in, and not otherwise subtracted from, FTI. The Department of Taxation has explained that the subtraction equals the net inclusion after offsetting the § 250 deduction, so Virginia removes the same net amount as Florida without a separate § 250 addition.

North Carolina reaches the same result through a pair of provisions that offset one another. Section 105-130.5(b)(3b) deducts from FTI any amount included under §§ 78, 951, 951A, or 965 of the Code, net of related expenses, which removes the inclusion. Section 105-130.5(a)(28) adds back the amount deducted under § 250, which is necessary because FTI reflects the inclusion only after the § 250 deduction reduces it. The two adjustments zero out the federal inclusion (§ 951A inclusion and its related § 250 deduction), resulting in the same net-cancellation effect in the North Carolina tax base as observed in Florida and Virginia.

Alternatively, a state that has not decoupled may reach the same result through a dividends-received deduction tied to the inclusion’s placement on the dividends schedule.

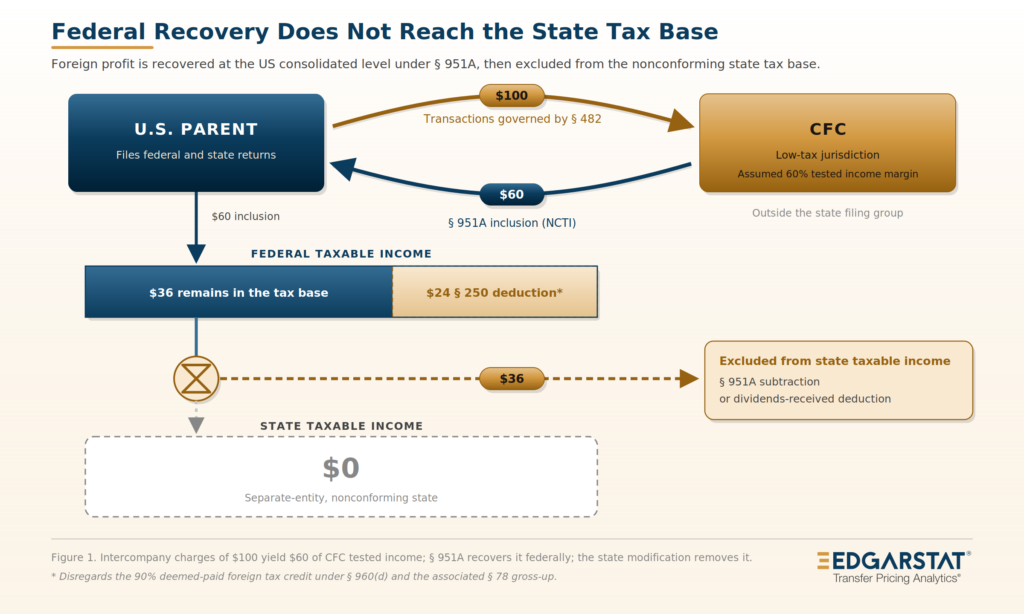

Figure 1 above illustrates the mechanics of how the NCTI on a $100 foreign related-party charge (e.g., services, finished or semi-finished goods, R&D) is recaptured in the federal tax base under the OBBBA regime. Many nonconforming states have statutes removing this income from the state tax base.

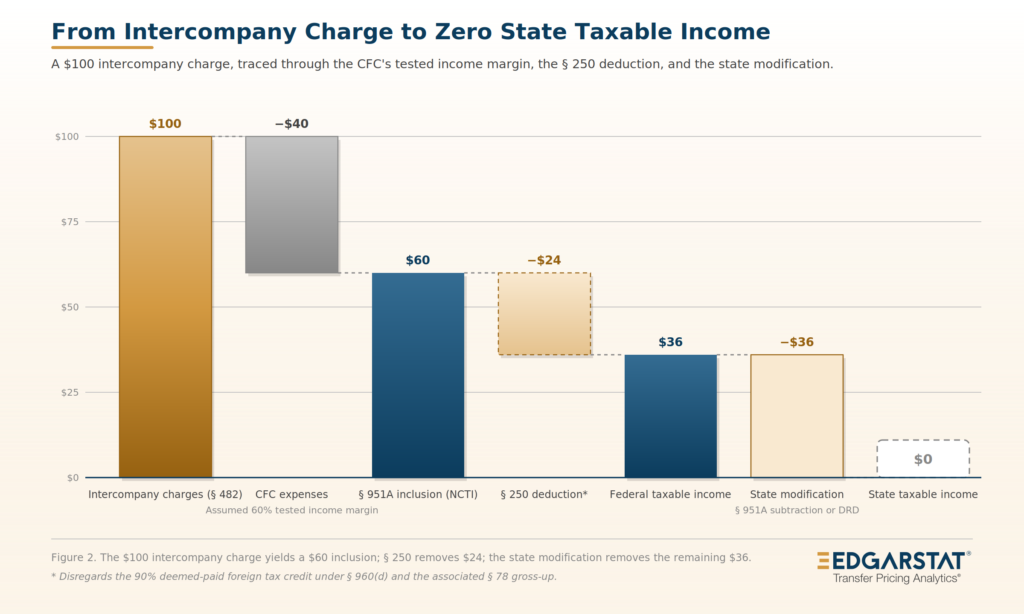

Figure 2 above illustrates the same scenario as in Figure 1, now in a waterfall format to visualize how the income recaptured from a $100 expense paid by the domestic filer to a foreign affiliate is reduced to $0 in the nonconforming state’s base.

At repatriation

The second stage occurs when the CFC distributes its earnings. Section 245A allows the domestic parent a deduction for the foreign-source portion of dividends received from a specified ten-percent-owned foreign corporation, and a conforming state inherits that deduction through FTI. Earnings that were previously included as subpart F income or NCTI return to the parent as previously taxed earnings and profits under § 959, without further federal tax and therefore without further state tax. Where the distribution is routed through a domestic intermediary (e.g., a holding company) rather than paid directly to the ultimate parent, the onward dividend between the domestic entities carries the domestic dividends-received deduction, and the corresponding state deduction removes it from the state base.

Earnings shifted to a CFC are therefore excluded from a separate-entity state’s base at both points, first when the attributed income is removed or never captured, and again when the cash returns under a deduction that the state inherits from the federal computation.

Existing state remedies to base erosion

A state confronted with this exposure faces a choice wider than the book’s two prescribed options. Many separate-entity states already possess statutory authority to address the regulatory gap predicted by the book. The existing state statutory authority includes reallocation of income among commonly controlled entities under direct conformity to § 482 or a similar arm’s-length analog, disallowance of specified related-party deductions under an add-back provision, compelled combined filing where intercompany transactions have shifted income, and alternative apportionment where the standard formula does not reflect the taxpayer’s business activity.

Conformity to the federal NCTI inclusion and WWCR remain available, but would require new legislation in most states. Meanwhile, the authorities listed below are already codified, so their application is a matter of administrative priority.

The following table records the principal related-party authority in twelve states:

Separate-entity states

| State | Statute | Mechanism |

|---|---|---|

| Alabama | Ala. Code § 40-2A-17 | § 482-style reallocation of income and deductions among commonly controlled entities to prevent evasion or clearly reflect income |

| Arkansas | Ark. Code § 26-51-805(e) | § 482-style reallocation among commonly controlled corporations |

| Florida | Fla. Stat. § 220.13 | Adjusted-federal-income conformity; § 220.13(1)(b) currently subtracts the § 951A inclusion from the base |

| Georgia | O.C.G.A. § 48-7-31(e) | Elimination of affiliate payments in excess of fair value and imputation of fair compensation for commodities sold or services performed for a parent or affiliate |

| Louisiana | La. R.S. 47:287.480(2) | Near-verbatim § 482 reallocation among commonly controlled businesses |

| Mississippi | Miss. Code § 27-7-37(2)(a)(ii) | Compelled combined return (pending regulations) where a preponderance of the evidence shows that intercompany transactions shifted income to a non-taxable affiliate |

| North Carolina | N.C. Gen. Stat. § 105-130.5A | Add-back, elimination, or adjustment of intercompany transactions that lack economic substance or are not at fair market value, escalating to compelled combination where adjustment is inadequate |

| South Carolina | S.C. Code § 12-6-2320 | Alternative apportionment in subsection (A), with a 2024 adjust-or-combine framework in subsection (B) |

| Tennessee | Tenn. Code § 67-4-2014(c) | § 482-style reallocation among commonly controlled businesses |

| Virginia | Va. Code § 58.1-446 | Equitable adjustment and compelled consolidation where intercompany arrangements improperly reflect the business done or Virginia taxable income earned in the Commonwealth |

Unitary combined reporting states

| State | Statute | Mechanism |

|---|---|---|

| Kentucky | Ky. Rev. Stat. § 141.205 | Disallowance of intangible expense, intangible interest, and management fees paid to related members, with a cap allowing deduction of other related-party costs only at the arm’s-length amount |

| West Virginia | W. Va. Code § 11-24-13a | Mandatory unitary combined reporting since 2009, with case-by-case authority to include the income and factors of an additional unitary member whose exclusion represents avoidance or evasion of tax |

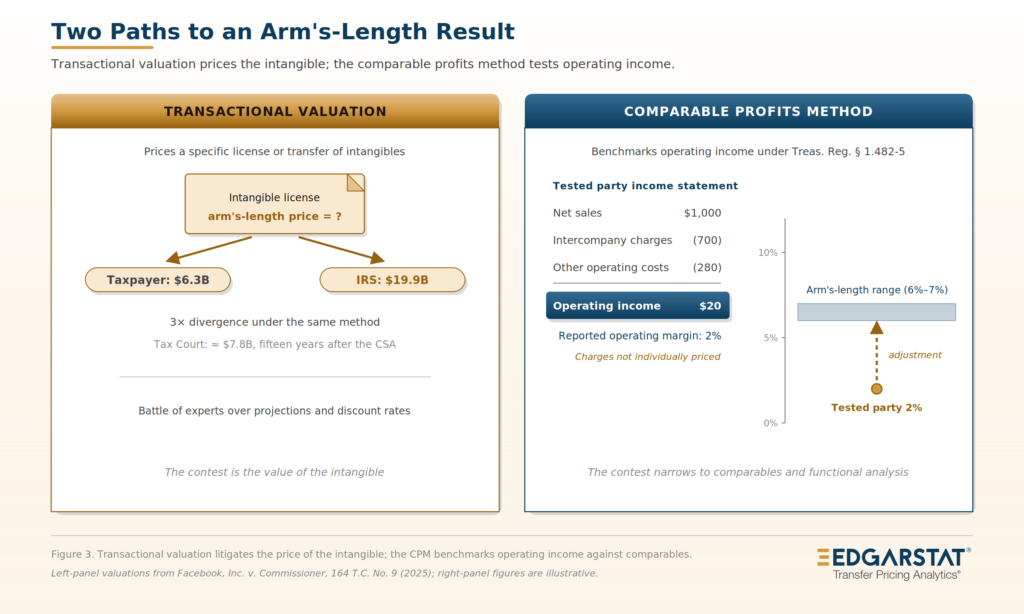

One distinction in the enforcement burden the MTC describes deserves recognition. The federal disputes underlying the book’s cost-and-delay narrative focused on intangibles valuation, contests over the arm’s-length price of a specific license or transfer. The authority surveyed above does not commit a state to the same exercise. A state may instead adjust the operating income of the domestic entity, tested against arm’s-length benchmarks drawn from comparable companies, in the manner of the comparable profits method under Treas. Reg. § 1.482-5. Under that approach, the intercompany charges need not be individually priced; if they leave the domestic entity with operating income below an arm’s-length return for its functions performed, assets employed, and risks assumed, the state’s adjustment restores the entity to the appropriate range at the level of operating income. A profits-based adjustment remains contestable, since comparables selection and functional analysis are litigable, but the contest focuses on the filer’s operating-level profitability rather than on transactional adjustments (e.g., the Facebook case).

Figure 3 below contrasts the federal transactional valuation disputes highlighted in the book with the operating-level remedy available to states.

Conclusion

A federal regulatory shift from transfer pricing enforcement to attribution would change the terms on which states have historically protected their corporate tax bases from erosion through international income shifting, whatever the ultimate pace of the enforcement changes the MTC anticipates. A separate-entity state that neither conforms to the federal inclusion of NCTI nor combines its foreign affiliates relies on federal transfer pricing enforcement that it does not control and cannot compel. Such a state may leave its exposure where it lies, or pursue the structural changes the book presents.

A third course requires no legislative action: most of the separate-entity states examined in this article already possess the statutory authority to adjust related party transactions, so the base erosion the book describes can be remedied through the administration of these existing statutes. The choice falls to the states to determine their enforcement priorities.

Sources: Multistate Tax Commission, Briefing Book, “Changes in Federal Taxation of Multinational Corporate Groups” (March 13, 2026); the state statutes cited in the table and in text; Virginia Department of Taxation Tax Bulletin 19-1; and the case decisions cited in text.